In today’s fast-evolving financial ecosystem, your credit profile plays a decisive role in shaping your borrowing power. Whether you are applying for a personal loan, home loan, or credit card, lenders rely heavily on your credit history to assess risk. One of the key indicators used in India and globally is the credit score, which has gained significant importance in 2026 as lending decisions become more data-driven and real-time.

While many borrowers are familiar with the cibil score, fewer fully understand how the credit scoring system works, how it differs, and why it is becoming increasingly influential in modern credit evaluation.

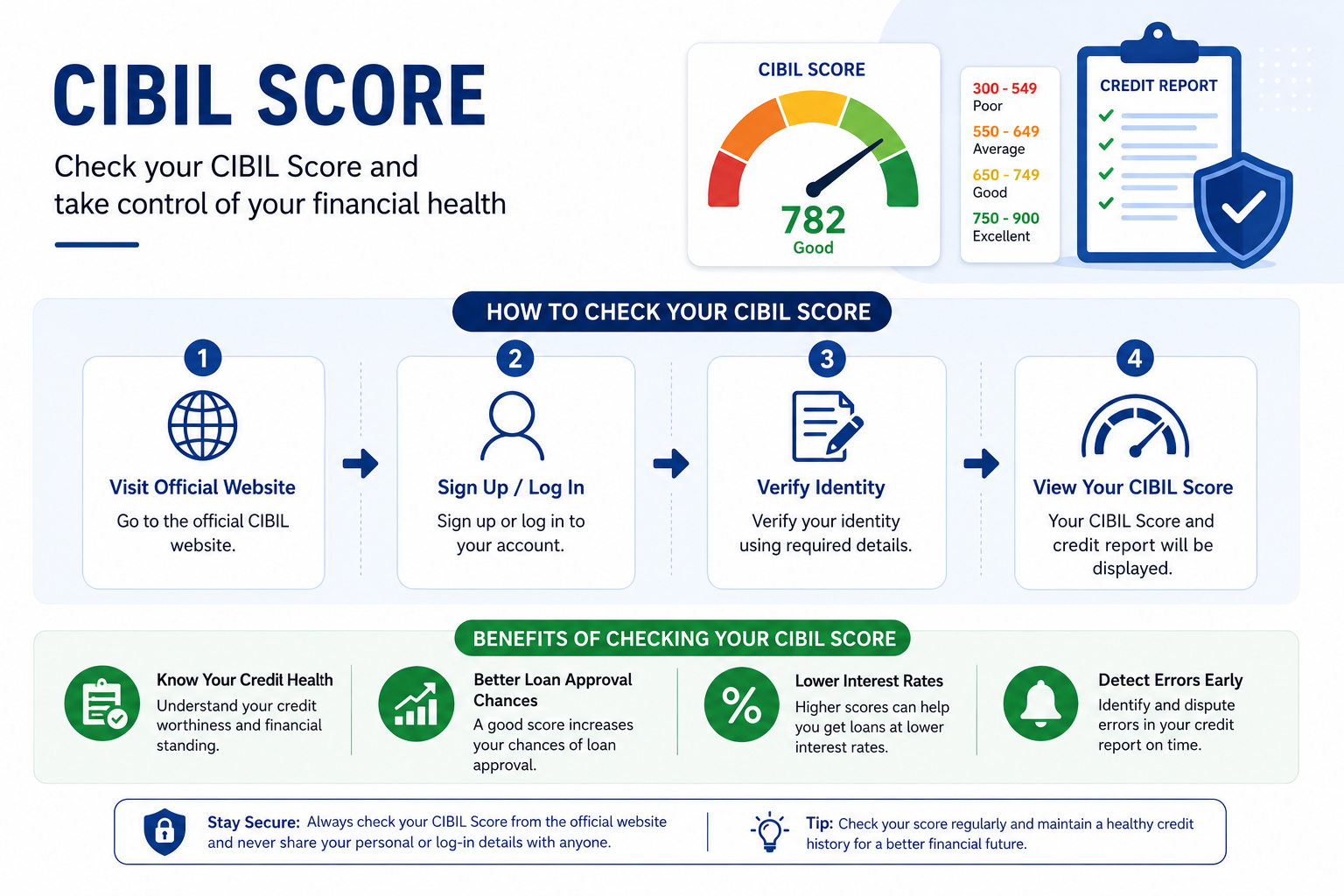

What is an Credit Score?

The credit score is a three-digit number ranging from 300 to 900 that reflects your creditworthiness. It is generated by , one of the leading global credit bureaus operating in India and several other countries.

This score is based on your credit behavior, including:

- Loan repayment history

- Credit card usage

- Outstanding debts

- Credit enquiries

- Length of credit history

A higher score indicates responsible financial behavior, while a lower score signals higher lending risk.

Why the Credit Score Matters in 2026

In 2026, lending has become more automated and AI-driven. Banks and financial institutions now rely on multiple credit bureaus instead of just one. The credit score has gained importance due to its advanced data modeling and real-time credit updates.

Here’s why it matters more than ever:

1. Faster Loan Approvals

Lenders now use data to instantly assess creditworthiness, leading to quicker approvals.

2. Better Risk Assessment

Advanced algorithms allow lenders to evaluate borrower risk more accurately.

3. Wider Acceptance

Many banks and fintech companies now consider scores alongside the cibil score for decision-making.

4. More Personalized Loan Offers

Borrowers with strong profiles may receive customized interest rates and offers.

Credit Score Range Explained

Understanding your score range helps you evaluate your financial standing:

- 800 – 900 (Excellent): Very high chances of approval with best interest rates

- 700 – 799 (Good): Strong credit profile with favorable terms

- 600 – 699 (Fair): Moderate risk; may face higher interest rates

- 300 – 599 (Poor): High risk; loan approvals may be difficult

A score above 750 is generally considered strong in 2026’s lending environment.

How Credit Score is Calculated

The credit score is calculated using multiple financial factors:

1. Payment History

Timely repayment of EMIs and credit card bills has the highest impact.

2. Credit Utilization Ratio

Using too much of your available credit limit negatively affects your score.

3. Credit Mix

A healthy combination of secured and unsecured loans improves your profile.

4. Credit Inquiries

Too many loan applications in a short time can reduce your score.

5. Credit Age

Older credit accounts help build trust with lenders.

Credit Score vs CIBIL Score

Many borrowers often compare the credit score with the cibil score, as both are widely used in India. While they serve the same purpose—assessing creditworthiness—there are some differences:

- Different Bureaus: and CIBIL are separate credit reporting agencies

- Scoring Models: Each uses slightly different algorithms

- Data Sources: Lenders may report data to one or multiple bureaus

- Score Variation: Your score and CIBIL score may not always match

Despite these differences, both scores are equally important in 2026. Many lenders now check both before making a decision.

Why Your Credit Score Can Affect Loan Approval

In 2026, financial institutions are becoming more cautious and data-driven. Your credit score helps lenders answer key questions:

- Are you likely to repay on time?

- How much credit risk do you represent?

- Have you managed debt responsibly in the past?

A strong score increases your chances of approval, while a weak score may lead to rejection or higher interest rates.

How to Improve Your Credit Score

If your score is not where you want it to be, you can improve it with disciplined financial habits:

- Pay all EMIs and credit card bills on time

- Keep credit utilization below 30%

- Avoid multiple loan applications at once

- Maintain a long and healthy credit history

- Regularly check your credit report for errors

Consistency is key—improving your credit score takes time but delivers long-term benefits.

Common Mistakes That Lower Your Score

Many individuals unknowingly harm their credit profile. Avoid these mistakes:

- Missing payment deadlines

- Maxing out credit cards

- Ignoring old unpaid dues

- Frequently closing credit accounts

- Applying for unnecessary credit

These behaviors can negatively impact both your credit score and cibil score.

Why 2026 is a Crucial Year for Credit Awareness

With the rise of digital lending platforms, instant loans, and AI-based credit underwriting, your credit score is now more important than ever. In 2026, financial decisions are increasingly automated, leaving little room for manual intervention.

This makes maintaining a strong bajaj finserv cibil score essential for:

- Home loans

- Personal loans

- Credit cards

- Business financing

- Buy-now-pay-later services

Final Thoughts

Your experian credit score is more than just a number—it is a reflection of your financial discipline and trustworthiness. In 2026, as lending becomes more advanced and competitive, maintaining a strong credit profile is essential for accessing better financial opportunities.

While the cibil score continues to remain widely used in India, ’s growing influence means borrowers must monitor both scores regularly. By practicing responsible credit behavior and staying financially aware, you can ensure a strong credit profile that supports your long-term financial goals.